In spite of and because of recent OPEC activity to cut production, oil markets have continued to be volatile in terms of price. In late November, NYMEX crude oil futures were at $45, and today they hover around the $50 mark. In the U.S., the Permian Basin continues to grow oil production. The Energy Information Administration's DPR projects a 27,000 barrels per day increase from November to December in the Permian, with the Niobrara region increasing by 2,000 barrels per day. In the Bakken and Eagle Ford, production is still declining. The following link is a short feature about Pioneer, a leading Permian producer, and Tim Dove's transition as the new incoming CEO: • "How Tim Dove Will Move Pioneer Natural Resources Forward" published in D CEO, December 2016. (The chart caption should say shale oil, not oil shale.)

Geopolitics and Energy Mash Up

Surprisingly, the geopolitics in play in my last post are not much different than today's. The Q&A below offers some insights into Putin's moves on the world stage. With low oil prices still lingering and whipsawing around, the green side of energy has seemingly decoupled from oil's tethers. In offering a balanced lineup of subject matter —from global security and shale gas to edgy academic research and energy market plays, the following new works are highlighted:

- A Q&A with Ambassador Pinkering on global hot spots. See the 11/06/15 entry.

- New findings that shale gas wells are not over-drilled.

- Re-freshed content and design of the Cox School faculty research site. (The profile about crowd-sourced investment research is interesting.)

- A look at Toyota's claim about conventional gas engines going by the wayside in 2050, and how various scenarios could present themselves.

- Finally, a couple of firm's reporting in the third quarter offer clues as to how various sides of the oil and gas business are faring: Halliburton here and Pioneer here. In a depressed pricing environment, firms are focused on strengths like never before.

Looking Back to See Ahead

To catch up with recent writings, I'm posting two items that capture noteworthy trends in oil markets: 1) "U.S. Shale Gale: A Whale Of A Tale, And Permian Walkabout," that speaks to U.S. producers' activities in light of the new normal in pricing; and

2) "Cartels, Sci-Tech And Breaking Bad: Oil Markets' New Normal?" offering more scenarios possible in oil markets than answers.

The upcoming OPEC meeting may offer little new information, as the strategy to pursue market share, particularly for the Saudis and Gulf states, continues to manifest. Geopolitics in the Middle East are in a perilous status quo.

While often writing about oil markets and U.S. shale resources, the advances in renewables, infrastructure developments (including U.S. midstream), and other energy and resource developments are being studied and considered. A recent article about global infrastructure firm Fluor captures some of the diversity in energy that overlays the global map. An excerpt follows since this article will be inaccessible in a couple of days:

Natural gas demand is expected to grow by 30% between 2014 and 2025 and production will increase by almost 40%, notes an IHS study. This demand is driven by power generation and industrial users. With low natural gas prices and ample NGL supply, the American Chemistry Council expects investment of $135 billion in 211 projects; this estimate was upped from a February 2014 estimate of $100 billion and 148 distinct investments.[i]

Fluor is also involved in the highly technical work of nuclear power plants, including their decommissioning. Recently, the company acquired 98% ownership of a nascent nuclear technology called NuScale. Majority-owned by Fluor, NuScale Power, LLC is developing a new kind of nuclear plant considered a safer, scalable version of pressurized water reactor technology, designed with natural safety features.

A big bet, Fluor believes NuScale could revolutionize the nuclear power industry and offer a $400 billion-dollar market.[7] In two decades, the business could be 'huge,' especially with their exclusive rights to build the smaller-scale, modular units. These 50-megawatt (MW) units can be stacked, like six packs, creating a 300 MW plant or more scaled-up plant based on the need. A recent Wall Street Journal article mentioned how the West, and particularly the U.S., is being usurped by China and Russia in nuclear build expertise. However Fluor may capitalize on the trend regardless of who leads the effort given their global footprint and ability to scale nuclear energy in diverse and new ways.

U.S. Energy Supply Alters Benchmarks and Trade

The Dallas Committee on Foreign Relations recently posted the inaugural publication of its "Global Themes Forum," an occasional series of articles, essays and thought pieces about topical global affairs issues. The first installment is a thought piece on global oil markets titled, "U.S. Energy Supply Alters Benchmarks and Trade Scenarios." See the item listed January 27,2015. And if the big picture isn't of concern, a dive into global oil markets after the Saudi succession, or how consolidation in the U.S. energy industry is beginning, may be of interest.

1) "Post-Saudi Succession, Oil Markets Seeking An Elusive Equilibrium" here.

2) The Energy Transfer merger between "family" members: "Energy Transfer Merger Creates Second Largest MLP, Scale Economies" here.

Oil Market Gyrations Creating an Altered Horizon

The timeframe of November through the first part of December saw levels of volatility in oil prices unseen for years. This article details some of the numbers supporting the shapeshifting market. But, in time, the fundamental drivers of supply, demand and geopolitics will clear up the tattered picture, as it always does. The OPEC decision to leave quotas intact created a tsunami effect for industry players. However, a slight bit of clarity is emerging as one large oilfield services firm notes some initial observations in production and investment activity around the world.

The Work Ahead on Greenhouse Gases: Mitigation and Investment

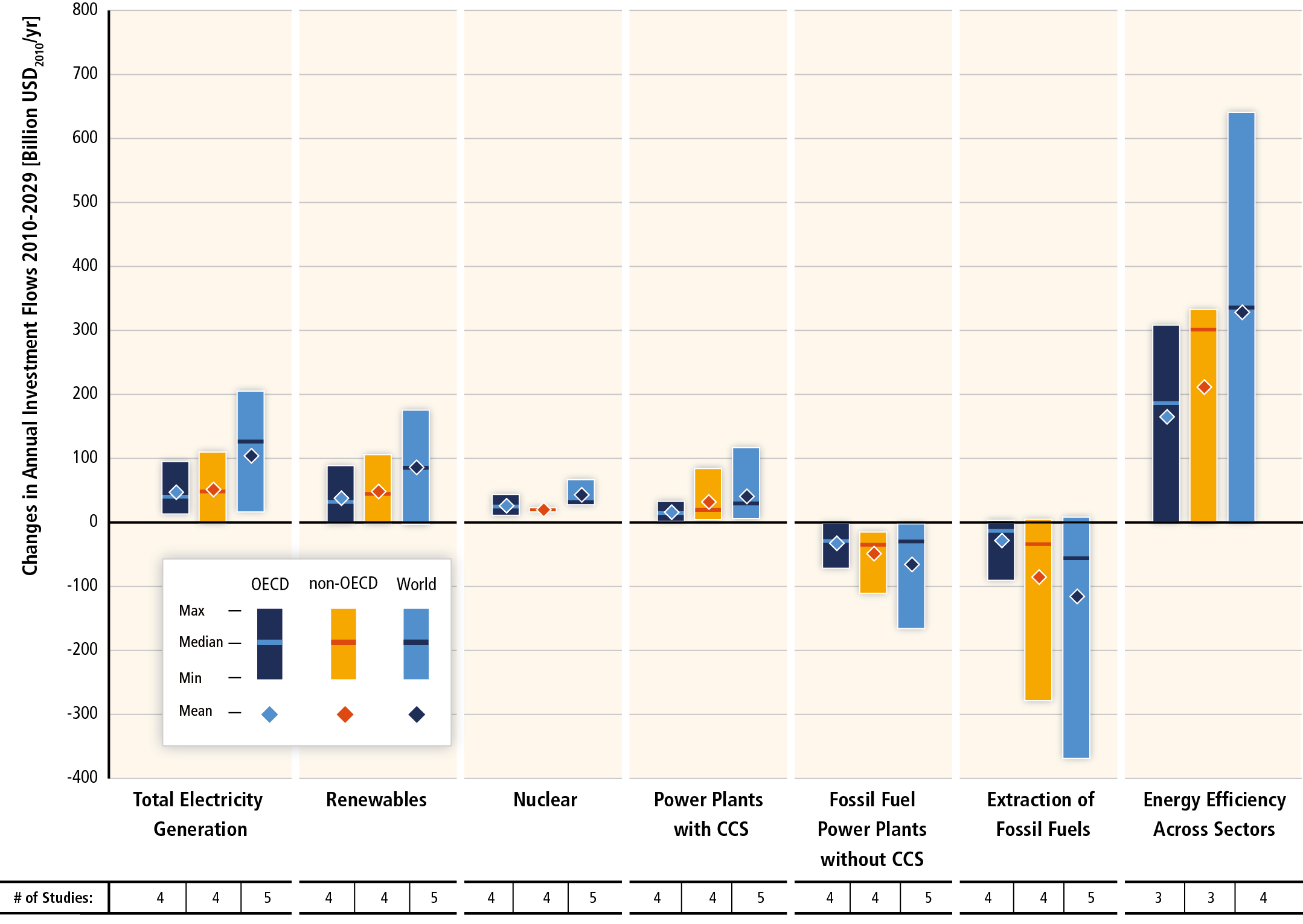

World-wide, the state of greenhouse gas emissions is abysmal. The two following graphics sum up the state of greenhouse gas emissions (GHG): how much we are emitting and the sources of origin. GHG emissions increased from 27 to 49 gigatons of CO2 equivalent per year between 1970 and 2010; the last decade was the highest in human history, which is not surprising. A gigaton is equal to one billion tons.

The Intergovernmental Panel on Climate Change says:

Globally, economic and population growth continue to be the most important drivers of increases in CO2 emissions from fossil fuel combustion. The contribution of population growth between 2000 and 2010 remained roughly identical to the previous three decades, while the contribution of economic growth has risen sharply.

In Asia, GHG emissions rose by 330% over the last four decades, reaching 19 GtCO2eq/year in 2010. The Middle East and Africa's GHG emissions grew 70%, Latin America by 57%, and advanced economies by 22%. In absolute terms, international transportation contributes a relatively smaller amount of GHG emissions, but they are growing rapidly. The increased use of coal since 2000 has reversed the slight decarbonization trends, they note.

(AFOLU is agriculture, deforestation, and other land use changes, a second largest contributor to GHG emissions.)

From an investment point of view, considerable reversals of investment in the non-OECD world would be needed to bring emissions into a range of stabilization in the "extraction of fossil fuels" category. Between the period 2010-2029, an average of approximately $300 billion per year, up to $600 billion, would need to be spent by both advanced and non-advanced economies in energy efficiency across sectors to stabilize emissions. Global total annual investment in the energy system is about $1.2 trillion. Annual incremental energy efficiency investments in transport, buildings, and industry is projected to increase by $336 billion, largely from modernizing equipment. (The charts are sourced from the IPCC's Fifth Assessment report, mainly from the Workgroup III section.)

Global Firm Flowserve Indicative of Resource and Infrastructure Trends

Flowserve Corp., a leading manufacturer and service provider of flow control systems, is poised to capture the resource-focused trends spanning the globe. As a global firm with a $9 billion capitalization, Flowserve is both geographically-diversified and diversified within energy infrastructure, water infrastructure and industrial sectors. The firm is poised to negotiate the dual-track energy developments in conventional and unconventional hydrocarbon trends as well as clean energy. Given population growth, resource-constraints, and climate change scenarios[i], their portfolio touches most of the underlying industrial processes that modern and modernizing societies require.  (The rest of the article can be viewed on Seeking Alpha for 30 days, when it will subsequently appear behind their paywall.)

(The rest of the article can be viewed on Seeking Alpha for 30 days, when it will subsequently appear behind their paywall.)

[i] Warren, Jennifer (2012). Targeting the Future: Smarter, Cleaner Infrastructure Development Choices, Human and Social Dimensions of Climate Change, Prof. Netra Chhetri (Ed).

A Week with Oil Markets (Updated)

As of October 23rd, a floor may have firmed up beneath oil prices in the low $80 range for WTI. Major oil field services firm Halliburton does not see signs of its customers altering production plans at present. Large independent producer Occidental Petroleum notes in its earnings call for the third quarter that they are not making any deviations from earlier plans in the Permian Basin. (See a more in-depth article about oil market fundamentals and market players, "Global Oil Markets: There and Back Again.") From last week, when the bottom was nowhere in sight, the oil market appears to be finding its equilibrium, rising up from the lower $80s for both WTI and Brent crude prices. This series of articles provides numerous charts of fundamentals, including what margins a few key Permian Basin players rely on to produce profitably:

- "Global Oil Markets Finding a New Groove?" Oct. 16th here.

- "Fundamentals of Pioneer, the Permian Basin, and Oil Prices," Oct.15th here.

- "Oil Market Karma Reversed?" Oct. 9th here. And an update to that article: "The OPEC Oil Market Gambit," Oct 14th here.

The expert insights in the "Global Oil Markets..." article are derived from the commenter very recently visiting Saudi Arabia.

The expert insights in the "Global Oil Markets..." article are derived from the commenter very recently visiting Saudi Arabia.

Oil Market Snapshots

Today, the Seeking Alpha article, "Oil Market Karma Reversed?" offers a look at the fundamentals driving, or that should be driving, the oil market. Of course, volatility is an aspect of the oil market across decades. The reversal part of the title relates to an earlier article from December, 2013 that relayed the effects being noticed from U.S. shale oil production, namely that U.S. production was moderating some of the price volatility given global supply outages that would normally have driven prices up. An October 2013 article discusses fundamentals and the Permian Basin, and chronicles how shale basins were producing. Given the fundamentals, markets have been potentially over-reacting in their heavy blows to oil and gas producers and midstream firms.

Reading the Texas Tea Leaves

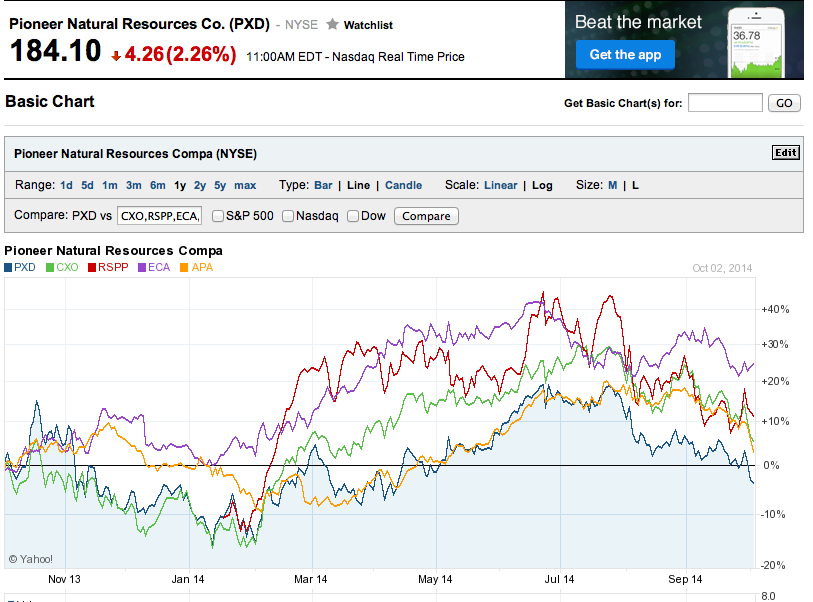

Given the breakneck-pace of shale oil production in the Bakken, Eagle Ford and Permian Basin, many stocks of the larger exploration and production firms drilling in these basins have been hammered as West Texas Intermediate (WTI) has tumbled.

Pioneer Natural Resources, a leader and top producer in the Permian and Eagle Ford, has seen its stock rise to $234.00 and fall back to $184.00, from virtually the same position as last year. $13.3 billion market cap Concho Resources (NYSE:CXO) followed the same trend as Pioneer. The smaller, newer additions such as RSP Permian (RSPP) recognized smaller price losses but it began from a lower price realization as a new IPO in January of 2014. When interviewing the CEO of RSP Permian in July, the sentiment about the Permian Basin's sustainability was positive.

According to Gray, he expects the Permian to continue producing when other basins slow down. Given its 'massive reserves, right geology, and history of oil and gas infrastructure,' these attributes combine for ease of operations and competitive advantages. The midstream segment of the oil and gas industry, charged with transporting, processing and storing resources, has been tracking the developments in production with some time lags. A recently published interview with CEO Kelcy Warren of Energy Transfer, a publicly-traded family of MLPs, or master limited partnerships, reveals one firm's continued growth and transformation as the industry continues to increase production. The midstream sector has made considerable investments in infrastructure to move the U.S. supplies around the country, and for export. (My report details some of the growth areas emerging from the midstream sector.)

Concerns about the oil supply growth with the potential for glut have been on the radar of numerous analysts for over one year. The prices of Brent crude and West Texas Intermediate (WTI) have fallen in tandem in the last few months. "WTI fell below $90 a barrel today for the first time in 17 months, extending this year’s decline to 9.9 percent," notes Bloomberg, and "Brent crude, fell 20 percent from its June peak to trade at $92.24 a barrel today on London’s ICE Futures Europe exchange." Weaker global demand and ample supply is a main culprit of the Brent crude decline; conversely the WTI declines are partially based on supply factors resulting from U.S. oil supply growth, along with the influences of Brent factors.